Blog

Qualified Opportunity Fund Minority Interest Valuation: How Discounts Cut Your Tax Bill

A qualified opportunity fund minority interest valuation can lower the taxable gain you recognize when your deferral period ends on December 31, 2026. This guide explains how discounts for lack of control and marketability work, what documentation your appraiser needs, and who can prepare a defensible report.

If you invested capital gains into a Qualified Opportunity Fund a few years ago, the deferral clock is now running out. The tax bill tied to that original gain comes due based on the fair market value of your LP interest, not the fund's stated net asset value, and for most minority investors, a properly supported valuation discount can meaningfully reduce that bill. Here is what happens at the end of the deferral period, why your position as a non-controlling limited partner matters, and how to get a defensible number before your CPA files.

What Happens When Your QOF Deferral Period Ends on December 31, 2026

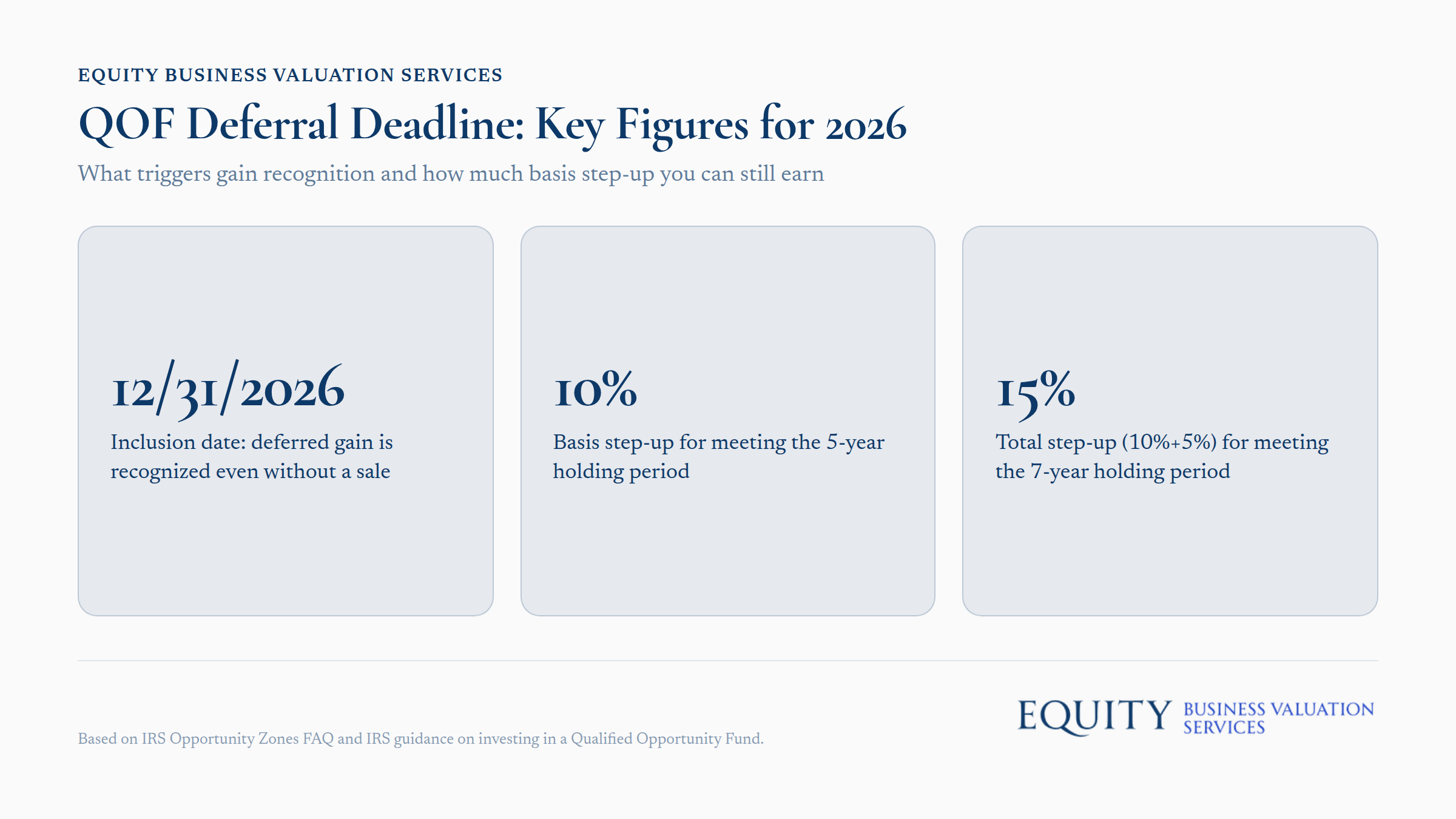

Under the Qualified Opportunity Zone rules, the capital gain you deferred by investing in a QOF is recognized on the earlier of two dates: the date you sell or exchange your QOF interest, or December 31, 2026. For nearly every investor still holding an interest, that means the 2026 date controls.

The IRS Opportunity Zones FAQ confirms that the deferral "lasts until the earlier of the date on which the investment in the QOF is sold or exchanged, or December 31, 2026." On that date, you must include the remaining deferred gain in income, whether or not you have actually sold anything.

The amount you report is not simply the original gain you deferred. Per the IRS guidance on investing in a Qualified Opportunity Fund, the taxable amount equals the lesser of:

- The original deferred gain, reduced by any 10% or 15% basis step-up you earned for meeting the 5-year or 7-year holding period, or

- The fair market value of your QOF interest on the inclusion date.

You then subtract your adjusted basis in the QOF interest from that number. If you held the investment at least 5 years before the end of 2026, your basis steps up by 10% of the deferred gain; a 7-year holding period adds another 5%, for a combined 15% permanent exclusion. As tax advisory guidance on 2026 opportunity zone reporting explains, the recognized gain is the difference between your adjusted basis and whichever is smaller, the reduced deferred gain or the interest's current fair market value.

This is the mechanic that makes valuation matter. If the fair market value of your LP interest on December 31, 2026 is lower than your original deferred gain (net of any basis step-up), that lower FMV becomes the number used to calculate your taxable gain. A supportable, below-NAV valuation is not a loophole; it is simply an accurate reflection of what your specific interest is actually worth to a buyer on that date.

Fair Market Value Is the Standard, Not the Fund's Reported NAV

Fair market value, for federal tax purposes, is generally defined as the price at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell, and both having reasonable knowledge of the relevant facts. This standard comes from a long-standing IRS revenue ruling on valuing property for tax purposes, and it applies to partnership interests just as it applies to closely held stock or real estate.

That distinction matters because most QOFs report a net asset value (NAV) to investors, calculated as the pro-rata share of the fund's underlying assets. NAV is a useful accounting figure, but it is not the same as fair market value for a specific limited partner's interest. A buyer stepping into your shoes as a non-controlling LP would not pay full pro-rata NAV; they would pay less, because of what they cannot do with that interest.

Why a Minority LP Interest Is Worth Less Than Its Pro-Rata Share of NAV

A minority, non-controlling interest in a QOF is typically valued below its pro-rata share of NAV because the limited partner cannot direct the decisions that create liquidity or control outcomes. This is standard business valuation theory, applied here to a partnership interest rather than a corporate share.

Two distinct, sequential discounts capture this gap:

- Discount for lack of control (DLOC): a reduction that reflects the LP's inability to control distributions, financing decisions, asset sales, fund liquidation timing, or management changes. A controlling interest can force a sale or a dividend; a minority LP interest generally cannot.

- Discount for lack of marketability (DLOM): a reduction that reflects the absence of a ready market to convert the interest into cash. There is no public exchange for QOF LP units, transfers are often restricted, and a buyer would demand a lower price to compensate for that illiquidity and the uncertain timeline to any exit.

These two discounts are not interchangeable and should not be combined into one blended number without support. DLOC addresses control; DLOM addresses liquidity. A qualified appraiser applies DLOC first, against the pro-rata NAV, and then applies DLOM to the resulting minority-interest value, since a buyer of an already-discounted minority stake still faces a separate marketability problem on top of the control problem.

What Drives the Size of the DLOC and DLOM Discounts

The size of each discount depends on the specific facts of the partnership agreement and the fund, not a rule-of-thumb percentage pulled from a prior deal. Several factors typically drive the analysis:

- Governance and voting rights: What can a limited partner actually vote on or veto under the partnership agreement? Limited or no voting rights on major decisions support a larger DLOC.

- Distribution policy and history: A fund that has never distributed, or that reserves full discretion over distribution timing to the general partner, supports a larger discount than one with a consistent, contractual distribution schedule.

- Transfer restrictions and rights of first refusal: Most LP agreements require GP consent to transfer units and may grant the fund or other partners a right of first refusal. These restrictions reduce marketability and support a larger DLOM.

- Holding-period lock-ups and redemption gates: A fund with no redemption feature and years remaining before an expected exit event is less marketable than one nearing a stated wind-down date.

- Underlying asset illiquidity: If the Opportunity Zone real estate is still under construction or in lease-up, the underlying fund-level fair market value itself may be discounted for development and leasing risk, before DLOC or DLOM are even layered on top. A stabilized, fully leased asset supports a very different starting NAV than a project mid-construction.

Each of these factors needs to be evaluated against the actual partnership agreement and fund financials, not assumed.

Does the IRS Require an Appraisal to Support a Discount?

No, the IRS does not require a formal appraisal to claim a reduced fair market value on a QOF interest. That said, a contemporaneous, independent appraisal is the strongest evidence available if the position is ever examined, since it documents the reasoning, the data reviewed, and the specific facts that justified the discounts applied.

A discount claimed without that supporting analysis, based on a generic percentage or a prior year's number, is much harder to defend. The discount has to be tied to the specific partnership agreement, distribution history, transfer restrictions, and underlying asset condition of your fund, not a borrowed figure from an unrelated deal.

How Equity Business Valuation Services Performs This Valuation

Our valuation team prepares QOF minority interest reports at fair market value, in accordance with the Uniform Standards of Professional Appraisal Practice (USPAP) published by The Appraisal Foundation. Our appraisers hold credentials with leading organizations such as the American Society of Appraisers, the National Association of Certified Valuators and Analysts, and the AICPA's Accredited in Business Valuation (ABV) credential.

We do not, and cannot, promise that the IRS will accept any specific discount percentage; no appraiser can guarantee that outcome. What we do prepare is a defensible, standards-compliant report built to meet the documentation expectations examiners look for: a clear standard of value, a reviewed data set, a reasoned control and marketability analysis, and a conclusion tied to the actual terms of your partnership.

As with all business valuation engagements, this work is performed remotely. There is no on-site visit required; the analysis is based on the fund's governing documents and financial records, which our team reviews and analyzes directly.

Pro tip: Start the valuation conversation with your CPA well before December 31, 2026. FMV has to be determined as of that specific date, and gathering fund-level documents from a GP can take longer than investors expect.

What We Need From You to Start the Engagement

To prepare a supportable QOF minority interest valuation, we typically request the following from the investor, their CPA, or their attorney:

- The limited partnership agreement: governing document showing voting rights, distribution policy, transfer restrictions, and any redemption provisions.

- Capital account statements and K-1s: to confirm your ownership percentage, contributions, and any distributions received to date.

- QOF financial statements: including the most recent balance sheet and any NAV reporting furnished to investors.

- Existing appraisals of the underlying Opportunity Zone real estate or QOZB assets: if the fund or GP has commissioned any, since these inform the entity-level value before discounts are applied.

- Distribution history: actual cash distributed to date, which supports (or undercuts) the marketability analysis.

The more complete this file is at the start, the faster we can produce a defensible conclusion of value tied to your specific December 31, 2026 inclusion date.

Who Can Help Me With This Valuation

If your accountant flagged a possible minority interest discount and pointed you toward finding "someone who does this," that is exactly the work our team performs. Equity Business Valuation Services prepares fair market value opinions on QOF LP interests directly for investors, and we work alongside the CPAs and attorneys managing the surrounding tax return and compliance work. We do not refer this out or subcontract the analysis; our credentialed valuation team handles the engagement from intake through final report. You can review our business valuation services or see current pricing before requesting a report.

Frequently Asked Questions

Q: Does the IRS require an appraisal to support a reduced fair market value on my QOF interest? No. There is no statutory requirement for a formal appraisal. However, a contemporaneous, independent valuation report is the strongest documentation available if your position is ever examined, since it shows the specific facts and reasoning behind the discount rather than an assumed percentage.

Q: Can a minority interest discount eliminate my tax liability entirely? No. The discount reduces the fair market value used in the calculation, which can lower your recognized gain, but it does not eliminate the underlying obligation to report deferred gain by December 31, 2026. Any basis step-up you earned from a 5-year or 7-year holding period is applied separately, as described in the IRS guidance on Qualified Opportunity Funds.

Q: What if my QOF invests in a property that's still under construction or lease-up? That affects the analysis at two levels. First, the underlying real estate's own fair market value may be discounted for development or lease-up risk, independent of your LP position. Second, the fund-level illiquidity that supports a DLOM is often more pronounced when the underlying asset has not yet stabilized, since there is no operating history to anchor a buyer's expectations.

Q: How is this different from a real estate appraisal? A real estate appraisal values the physical property itself. A QOF minority interest valuation values your specific limited partnership unit, which sits behind the fund's ownership structure, governance terms, and transfer restrictions. The real estate's value is an input into the analysis, but the control and marketability discounts are applied at the LP-interest level, not the property level.

Q: Do I need this valuation every year, or just once? For most investors, the valuation that matters is the one dated as of the inclusion event, generally December 31, 2026, since that is the date used to calculate the recognized gain. If you sold or exchanged your interest earlier, that earlier date would control instead.

This article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. Readers should consult a qualified attorney or CPA regarding their specific circumstances.